Introduction

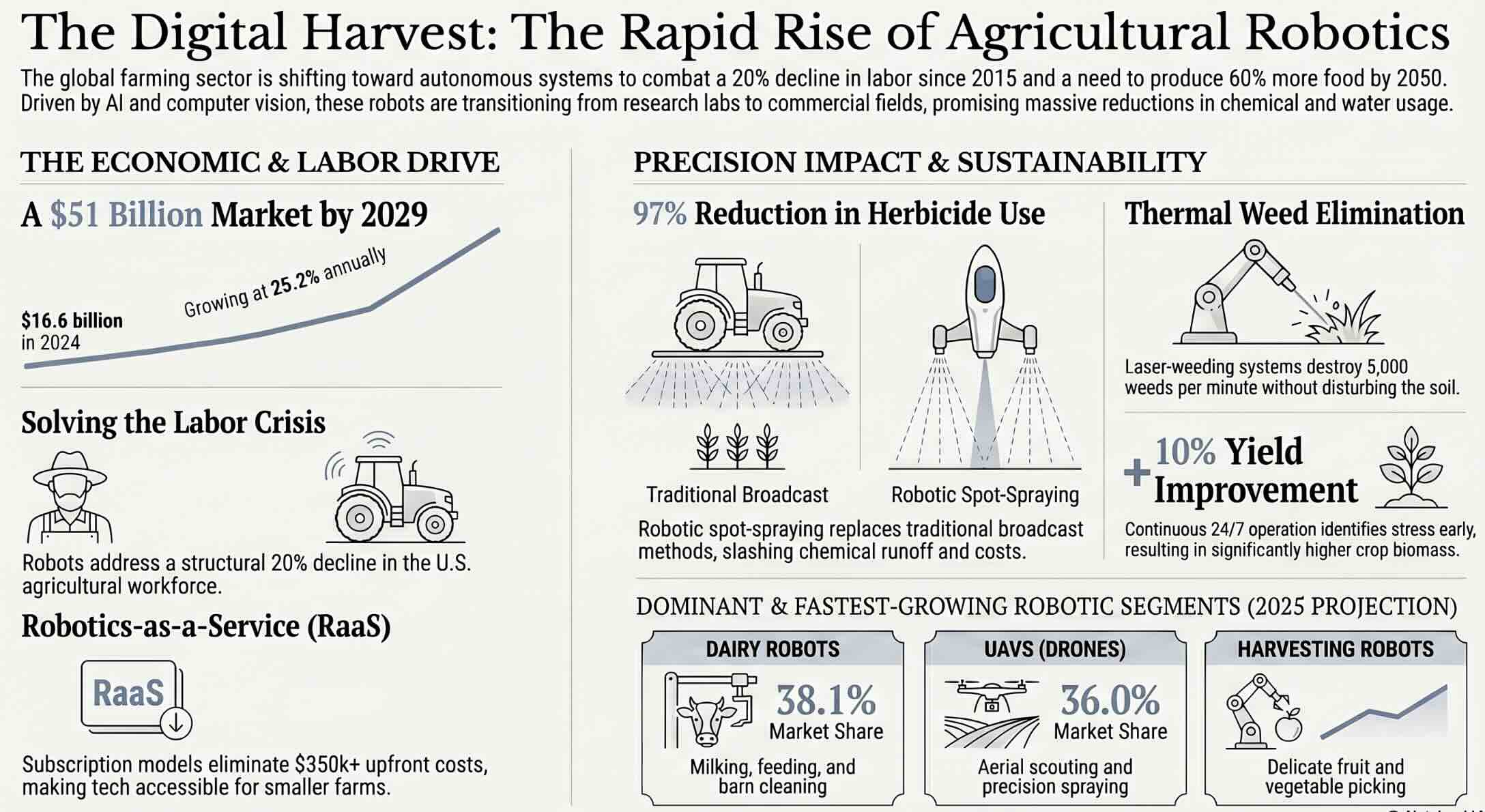

The global farming sector is entering a period of rapid transformation as autonomous machines take on tasks that once required intensive manual labor. According to MarketsandMarkets, the agricultural robots market was valued at approximately USD 16.6 billion in 2024 and is projected to reach USD 51 billion by 2029, growing at a compound annual growth rate of 25.2%. Labor shortages across the United States, Europe, and parts of Asia have pushed farming operations to seek automated alternatives at an unprecedented pace. The convergence of artificial intelligence, computer vision, and advanced sensor technologies has made it possible for robots to plant, weed, harvest, and monitor crops with remarkable precision. These machines are no longer confined to research labs or pilot programs; they are working in commercial fields around the world today. Farm operators who once relied entirely on seasonal workers and traditional tractors now have access to platforms that run on solar energy, navigate autonomously, and reduce chemical inputs by significant margins. The question is no longer whether robots belong on the farm, but how quickly the agricultural sector can scale their deployment to meet the challenges of a growing global population.

Quick Answers on Agricultural Robots

How much do agricultural robots cost?

Prices range from $18,000 for spray drones to $350,000 or more for large-scale autonomous weeding platforms, with robotics-as-a-service models making them accessible to smaller farms.

What are agricultural robots?

Agricultural robots are autonomous or semi-autonomous machines that use AI, sensors, and computer vision to perform farming tasks like planting, weeding, harvesting, and crop monitoring with minimal human intervention.

Why are agricultural robots important?

They address critical labor shortages, reduce chemical use by up to 95%, improve crop yields through precision application, and help farmers produce more food sustainably on existing farmland.

Key Takeaways

- High upfront costs, lack of interoperability standards, and ethical concerns around job displacement remain significant barriers that the industry must address for equitable adoption.

- The agricultural robots market is growing at over 20% annually, driven by structural labor shortages and the need for sustainable food production at scale.

- Robotic weeding and targeted spraying systems can reduce herbicide use by 50% to 97%, cutting input costs and lowering environmental impact for farmers of all sizes.

- Autonomous tractors, drones, and harvesting platforms are transitioning from pilot programs to full commercial deployment across North America, Europe, South America, and Asia Pacific.

Table of contents

- Introduction

- Quick Answers on Agricultural Robots

- Key Takeaways

- Defining Agricultural Robots

- Why Farms Need Autonomous Machines Right Now

- Types of Robots Reshaping Field Operations

- The AI and Sensor Stack Powering Precision Agriculture

- How Robotic Weeding Is Eliminating Herbicide Dependence

- Autonomous Tractors and the Shifting Role of the Farmer

- Drones and Aerial Intelligence for Crop Management

- Harvesting Robots and the Challenge of Gentle Handling

- Environmental Benefits of Precision Robotic Farming

- Regional Adoption Patterns Across Key Markets

- Robotics-as-a-Service and the Economics of Access

- Data Ownership and Privacy in Connected Farming

- Ethical Questions Around Labor Displacement and Rural Communities

- Safety Standards and Regulatory Gaps

- From Pilot Projects to Full-Scale Deployment

- Robotics in Controlled Environments and Vertical Farms

- Multi-Robot Fleet Coordination and Swarm Intelligence

- The Investment Landscape and Venture Capital Trends

- What Farmers Should Know Before Adopting Robotic Systems

- The Road Ahead for Agricultural Robotics

- Key Insights

- Real-World Examples

- Case Studies

- Frequently Asked Questions on Agricultural Robots

Defining Agricultural Robots

Agricultural robots are autonomous mechatronic platforms designed to execute farming operations such as sowing, spraying, weeding, harvesting, phenotyping, and soil monitoring with minimal or zero human intervention, using AI and robotics integration to achieve precision, efficiency, and sustainability in food production.

Agricultural Robot ROI Calculator

Estimate your potential savings and payback period by adjusting your farm’s parameters.

Projected Annual Impact

Why Farms Need Autonomous Machines Right Now

The agricultural workforce in the United States has declined by roughly 20% since 2015, and that trend is accelerating rather than stabilizing. In April 2025, only 637,000 hired crop workers were counted across the country, even as the temporary worker visa program issued over 310,000 visas in the prior year. This shortfall is not a seasonal blip or a regional inconvenience; it represents a structural shift in the labor market that traditional recruitment cannot solve. Younger generations are moving away from farming communities, drawn toward urban employment opportunities that offer higher wages and more predictable schedules. Climate change is compounding these challenges by making field work more physically demanding, with extreme heat events increasing the health risks associated with outdoor labor. The combination of a shrinking workforce and rising food demand means that farming operations must automate or risk falling behind in their ability to feed a population that will need 60% more food by 2050.

Farms across Europe and Japan face similar pressures, with aging populations and urbanization depleting the rural labor pool at alarming rates. The United Kingdom government invested £12.5 million in robotics and automation projects in September 2023 to enhance sustainable farming and support food security. Japan has long been a leader in robotics adoption due to its demographic crisis, and its government actively subsidizes autonomous agricultural equipment for small and mid-sized operations. These global trends are not isolated phenomena; they reflect a universal reality that food production systems everywhere must evolve. Autonomous machines offer a path forward by handling repetitive and physically demanding work around the clock without fatigue. The economic case for automated farming grows stronger each year as labor costs rise and robotic technology becomes more capable and accessible.

Types of Robots Reshaping Field Operations

Agricultural robots fall into several distinct categories, each designed to address specific tasks within the farming cycle. Autonomous tractors represent one of the most visible categories, with companies like John Deere, CNH Industrial, and formerly Monarch Tractor developing platforms that can plow, sow, and haul without a human driver in the cab. Unmanned aerial vehicles, commonly known as drones, have become the dominant product category by revenue share, accounting for approximately 36% of the market in 2025. These drones equipped with NDVI and thermal sensors can survey hundreds of acres per day, detecting pest infestations, irrigation problems, and nutrient deficiencies from the air. Weeding robots represent another rapidly growing category, with companies like FarmWise, Carbon Robotics, and Naïo Technologies building platforms that use computer vision to distinguish crops from weeds and remove unwanted plants mechanically or with targeted laser pulses. Harvesting robots are projected to grow at a compound annual growth rate of 18.9% between 2026 and 2031, making them the fastest-growing segment in the market.

Dairy robots have already achieved widespread adoption, dominating the market with a 38.1% revenue share in 2024 by automating milking, feeding, and barn cleaning operations. Milking robots alone accounted for 29.9% of the total market by application, driven by the global expansion of dairy farming and the chronic difficulty of hiring workers for early morning and late night milking shifts. Livestock monitoring systems use IoT sensors and AI algorithms to track animal health, movement patterns, and feeding behavior in real time. Phenotyping robots move through research plots and commercial fields to measure plant characteristics at a level of detail that human scouts could never match. The diversity of robot applications reflects the complexity of modern agriculture itself, where no single machine can address every challenge across different crops, climates, and farm sizes.

Multi-purpose platforms are emerging as a key trend for 2026 and beyond, with manufacturers building modular robots that can switch between planting, fertilizing, and weeding attachments depending on the season. This approach reduces the total cost of ownership for farmers who would otherwise need to purchase separate machines for each task. Specialty crop producers growing wine grapes, berries, and leafy greens have been early adopters of compact robotic platforms that navigate between narrow rows without damaging delicate plants. The modular design philosophy also extends to software, where open APIs allow third-party developers to build custom applications on top of existing robotic hardware.

The AI and Sensor Stack Powering Precision Agriculture

Modern agricultural robots rely on a sophisticated technology stack that combines multiple forms of perception, decision-making, and actuation. Machine vision systems using RGB, multispectral, and hyperspectral cameras enable robots to identify individual plants, assess ripeness, detect disease symptoms, and distinguish crops from weeds with high accuracy. Deep learning algorithms process these visual inputs in real time, allowing the robot to make split-second decisions about whether to spray, pick, or leave a particular plant untouched. Carbon Robotics, for example, recently introduced its Large Plant Model containing 150 million labeled plants, enabling its LaserWeeder to begin operating in any field or crop within minutes rather than requiring extensive calibration. LiDAR sensors create three-dimensional maps of the terrain and plant canopy, helping robots navigate uneven ground and avoid obstacles like rocks, irrigation equipment, and field workers.

GPS and RTK satellite navigation systems provide centimeter-level positioning accuracy, allowing robots to follow precise paths through fields and return to the exact same locations for repeated monitoring over the growing season. Machine learning algorithms analyze the vast quantities of data collected during each pass through the field, identifying patterns in soil moisture, plant growth rates, and pest populations that inform future management decisions. Soil sensors embedded in robotic platforms measure pH levels, nutrient concentrations, and compaction depth as the machine moves, generating detailed maps that guide variable-rate application of fertilizers and amendments. The fusion of these sensor modalities creates a perception system far more comprehensive than any individual technology could achieve alone, giving robots a multi-dimensional understanding of the agricultural environment.

Edge computing capabilities allow robots to process sensor data locally rather than relying on cloud connections that may be unreliable in remote agricultural settings. The software platforms behind these robots, such as Solinftec’s ALICE system, aggregate millions of data points per month to create continuously improving AI models that adapt to local conditions, crop varieties, and weed species. This data-driven approach transforms the robot from a simple tool into an intelligent agent that learns and improves with every pass through the field, making agricultural decision-making deterministic rather than predictive.

How Robotic Weeding Is Eliminating Herbicide Dependence

The transition from chemical weed control to robotic weeding represents one of the most impactful shifts in modern agriculture. Robotic weeding platforms use computer vision to identify weeds at the individual plant level and then remove them using mechanical tools, targeted herbicide micro-doses, or high-powered laser pulses. Carbon Robotics’ LaserWeeder can eliminate approximately 5,000 weeds per minute using thermal energy that destroys the plant without disturbing the soil or leaving chemical residues. The economics of robotic weeding are becoming increasingly competitive with traditional chemical approaches, particularly as herbicide-resistant weed populations spread and organic premiums of $500 to $2,000 per acre make chemical-free production more profitable for crops like strawberries and lettuce. Solinftec’s Solix Sprayer robots demonstrated herbicide reductions of up to 97% in initial trials during their first commercial season in the United States, while also conserving approximately 72,000 gallons of water.

The environmental benefits extend beyond chemical reduction alone, as lightweight robotic platforms cause significantly less soil compaction than conventional tractors towing heavy sprayer equipment. Solix robots operate on solar-charged batteries and can work 24 hours a day, covering up to 100 acres of farmland per day depending on field shape and terrain. This continuous operation means that weeds are caught at their earliest growth stages, before they can compete with crops for water, nutrients, and sunlight, resulting in up to 10% more biomass and potential yield improvement. The approach aligns with growing consumer demand for food produced with fewer chemicals, regulatory pressure to restrict certain herbicide formulations, and farmer desire to maintain long-term soil health.

Traditional broadcast spraying applies herbicides uniformly across an entire field regardless of where weeds actually grow, wasting product and exposing beneficial organisms to unnecessary chemical contact. Robotic spot-spraying and mechanical removal target only the plants that need treatment, reducing the total volume of active ingredients entering the ecosystem. This precision approach also slows the development of herbicide resistance by ensuring that fewer weed populations are exposed to selection pressure from chemical applications over time. The shift from blanket application to plant-level precision represents a fundamental change in how farmers think about weed management.

Autonomous Tractors and the Shifting Role of the Farmer

The autonomous tractor segment has attracted enormous investment and attention, with major manufacturers racing to deliver fully driverless platforms that can operate independently across large-scale broadacre farms. John Deere launched its AutoTrac GPS steering system in 2003 and has continued building toward full autonomy with its 8R autonomous tractor kit, which retrofits existing equipment with sensors, cameras, and AI-driven navigation capabilities. CNH Industrial, the parent company of Case and New Holland, has developed autonomous tractor concepts designed for large-scale broadacre operations, though commercial availability remains limited as of mid-2026. The fully autonomous tractor promises to free farmers from hours of repetitive driving, allowing them to focus on strategic decision-making, crop planning, and business management rather than sitting behind a steering wheel.

The path to fully autonomous tractors has not been without setbacks, as the industry learned from the cautionary tale of Monarch Tractor. Once valued at over half a billion dollars and backed by more than $240 million in funding, Monarch laid off its entire workforce in late 2025 and vacated its California headquarters by early 2026. The company’s electric, driver-optional smart tractor had generated significant excitement, but the gap between technological promise and commercial viability proved too wide to bridge with the capital available. This collapse underscores a critical lesson for the agricultural robotics industry: innovative technology alone does not guarantee market success without a sustainable business model, reliable supply chains, and realistic timelines for farmer adoption. Other companies have taken note, adopting more cautious approaches to commercialization that prioritize incremental capability releases over ambitious leaps to full autonomy.

The role of the farmer is evolving from manual operator to fleet manager and data analyst as autonomous systems become more capable. Farmers who adopt autonomous tractors still need to define field boundaries, set operational parameters, and monitor performance remotely through mobile applications and dashboards. The relationship between automation and human expertise is not one of replacement but of augmentation, where the machine handles execution while the farmer provides judgment, context, and strategic oversight that no algorithm can fully replicate.

Drones and Aerial Intelligence for Crop Management

Drones have emerged as the most widely adopted category of agricultural robots, with their relatively low entry cost and immediate return on investment making them accessible to farms of all sizes. A professional agricultural drone like the DJI Agras T50 costs approximately $18,000, a fraction of the investment required for ground-based autonomous platforms. These machines can cover 500 acres per day at a cost of $3 to $8 per acre, performing precision spraying, seeding for reforestation, and detailed crop health assessments using normalized difference vegetation index imagery. Drone-based monitoring detects problems such as pest infestations, nutrient deficiencies, and irrigation failures days or weeks before they would be visible to a human scout walking the field, giving farmers critical time to intervene before yield losses become irreversible. Companies already leveraging drone delivery technology for logistics are now extending these capabilities to agricultural applications.

Thermal imaging cameras mounted on drones can identify water stress in plants by measuring canopy temperature differences that correlate with transpiration rates. Multispectral sensors capture light reflected by plants across wavelengths invisible to the human eye, revealing patterns of chlorophyll content, biomass density, and early disease symptoms. These aerial perspectives transform farm management from a reactive practice into a proactive one, where data-driven insights guide every decision from planting to harvest. The combination of drone scouting with ground-based robotic action creates an integrated system where aerial intelligence directs precise interventions at the plant level.

Regulatory frameworks for agricultural drone operations vary significantly across countries, with some nations permitting beyond-visual-line-of-sight flights for farming applications while others impose strict altitude and proximity requirements. The United States Federal Aviation Administration has been gradually expanding the conditions under which agricultural drones can operate autonomously, recognizing the unique characteristics of rural airspace. As regulations mature and battery technology improves, drones will play an even larger role in agricultural automation by covering more ground with fewer recharging interruptions.

Harvesting Robots and the Challenge of Gentle Handling

Harvesting represents the most technically demanding application for agricultural robots, requiring a combination of perception, dexterity, and speed that pushes the boundaries of current robotics technology. The challenge of picking ripe fruit without bruising it demands end-effectors that can grip with the gentleness of a human hand while operating at speeds that make economic sense for commercial operations. Soft-grip mechanisms and machine-vision cameras work together to track fruit ripeness, position the gripper accurately, and apply just enough pressure to detach the fruit from the plant without damaging it. Laser targeting systems further reduce bruising and boost pack-out rates for delicate crops like berries, stone fruits, and tomatoes. Companies like Agrobot have developed autonomous fruit harvesting machines with precision picking systems tailored to strawberry operations, where labor costs are among the highest in all of agriculture.

Orchard platforms that previously moved human workers through rows of apple and peach trees are being retrofitted with robotic arms that can pick fruit faster and more consistently than seasonal laborers. Venture funding is accelerating commercial pilots across major growing regions in California, Washington, and New South Wales, Australia, with service providers beginning to guarantee per-acre cost parity with seasonal labor by the third season of deployment. Controlled-environment agriculture, including greenhouse and vertical farm operations, presents a more structured setting where harvesting robots can achieve higher accuracy and throughput because the growing conditions are predictable and standardized. Robots tailored to greenhouse tomatoes, cucumbers, and leafy greens are expanding the addressable market for harvesting automation beyond traditional open-field agriculture.

The economics of harvest robotics are shaped by the premium that fresh produce commands compared to grain crops, where combine harvesters have long been fully mechanized. Fruit and vegetable operations face the highest labor costs and the greatest vulnerability to worker shortages, making them natural candidates for robotic harvesting despite the technical difficulty. The evolution of food robotics extends from field to processing facility, where sorting, packaging, and quality inspection robots are becoming standard equipment in modern packinghouses.

Environmental Benefits of Precision Robotic Farming

Robotic farming offers measurable environmental benefits that go beyond simple efficiency gains, contributing to a more sustainable model of food production. Precision application of inputs means that fertilizers, herbicides, and pesticides are delivered only where and when they are needed, reducing runoff into waterways, minimizing harm to beneficial insects like pollinators, and lowering greenhouse gas emissions associated with chemical manufacturing and transport. Solinftec’s Solix robots have demonstrated herbicide reductions of up to 95% in post-emergence applications and 92% in desiccation and pre-planting operations across commercial farming operations in Brazil and the United States. Lightweight robotic platforms exert far less ground pressure than conventional tractors, reducing soil compaction that degrades root development, water infiltration, and long-term soil fertility. Electric-powered agricultural robots eliminate diesel emissions from field operations, contributing to the decarbonization of a sector responsible for roughly 10% of global greenhouse gas output.

Water conservation is another significant benefit, as robots equipped with soil moisture sensors and weather data can optimize irrigation timing and volume at the individual plant level rather than flooding entire sections of a field. The data collected by robotic platforms during their continuous operation creates detailed records of input usage, yield outcomes, and environmental conditions that support sustainability reporting and certification for organic and regenerative farming programs. AI and climate change mitigation intersect directly in agricultural robotics, where smarter machines translate into lower resource consumption and reduced ecological impact per unit of food produced. The environmental argument for agricultural robots strengthens as consumer, regulatory, and investor pressure on the food system intensifies.

These environmental gains are not theoretical projections; they have been measured in commercial field conditions by multiple independent studies and corporate sustainability reports. The challenge lies in scaling these benefits from early adopter farms to the broader agricultural sector, where cost barriers and knowledge gaps slow the transition. Governments and non-governmental organizations can accelerate this process by incorporating robotic precision farming into climate mitigation strategies, agricultural extension programs, and sustainability incentive frameworks.

Regional Adoption Patterns Across Key Markets

North America dominates the agricultural robots market, accounting for approximately 36% to 38% of global revenue in 2025, driven by acute labor shortages, large average farm sizes, and strong venture capital investment in agtech startups. The United States grain belt and California’s specialty crop regions are primary adoption zones, where the economic case for automation is most compelling due to high labor costs and the availability of technical support infrastructure. Canada has emerged as a testing ground for scouting robots, with companies like Solinftec conducting successful pilot programs that validated weed identification and pest monitoring capabilities in Canadian growing conditions. The Asia Pacific region is projected to be the fastest-growing market through 2031, with a compound annual growth rate of approximately 20.8% driven by government subsidies, labor shortages, and rapid technological modernization in Japan, China, South Korea, and India.

Japan stands out as a unique case where demographic necessity has made agricultural robotics adoption a national priority, with government programs actively subsidizing autonomous equipment purchases for aging farmers who can no longer perform physically demanding work. China’s massive investment in smart farming technologies and rural modernization programs is creating a vast market for robotic platforms adapted to rice paddies, vegetable production, and orchard operations. Europe’s adoption patterns are shaped by a combination of strong environmental regulations that incentivize chemical reduction, generous research funding through programs like the European Union’s Robs4Crops initiative, and a tradition of small to mid-sized family farming that requires robots designed for compact field operations. Latin America, particularly Brazil, has become a proving ground for large-scale robotic deployment, with Solinftec deploying its Solix platforms across the country’s vast soybean, corn, and sugarcane operations to demonstrate that autonomous agricultural robots can work at the scale the global food system demands.

Africa and South Asia represent largely untapped markets where smallholder farming dominates and robotic adoption is limited by infrastructure constraints, capital availability, and the need for technology adapted to local crops and conditions. The robotics-as-a-service business model, which converts capital cost into subscription payments, may prove essential for bringing automation to these regions without requiring farmers to make large upfront investments that their cash flows cannot support.

Robotics-as-a-Service and the Economics of Access

The high upfront cost of agricultural robots remains the single largest barrier to widespread adoption, particularly among small and mid-sized farm operations that lack the capital reserves of large agribusiness enterprises. A robotic weeding platform like the FarmWise Titan costs approximately $350,000, and an autonomous tractor kit from John Deere can exceed $500,000 when combined with the base tractor, placing these technologies out of reach for many farmers who would benefit most from automation. The robotics-as-a-service model addresses this gap by allowing farmers to access robotic capabilities through subscription payments, per-acre fees, or seasonal rental agreements that convert fixed capital costs into variable operating expenses. This approach mirrors the software-as-a-service model that transformed the technology industry by making enterprise tools accessible to businesses that could not afford large upfront license fees.

Service providers operating under this model deploy and maintain robotic fleets on behalf of farmers, handling everything from logistics and calibration to software updates and mechanical repairs. The farmer pays only for the work performed, reducing financial risk and eliminating the need for specialized technical expertise to operate and maintain complex robotic systems. This democratization of access is particularly important for the small and mid-sized farms that produce a significant share of the world’s food supply but have historically been excluded from the benefits of advanced agricultural technology. Cloud-based platforms that integrate satellite imagery, weather data, and robotic fleet management are making it possible for farmers to monitor and direct operations from a smartphone, regardless of their technical background.

The economics of robotics-as-a-service become more attractive as robot utilization rates increase, since service providers can amortize the cost of expensive hardware across multiple clients and growing seasons. The model also creates incentives for continuous improvement, as providers who deliver better outcomes attract and retain more clients. For a 500-acre vegetable operation, deploying robotic weeding and drone monitoring through a service model can save over $150,000 annually, with payback periods of approximately 2.5 years compared to traditional labor-intensive approaches.

Data Ownership and Privacy in Connected Farming

As agricultural robots collect millions of data points per month about field conditions, crop performance, and farming practices, questions about who owns this data and how it can be used have become increasingly urgent. Every pass through a field generates detailed records of soil health, plant populations, weed density, pest presence, and input applications that have significant commercial value beyond the individual farm. Robot manufacturers and service providers often retain rights to aggregate and analyze this data to improve their algorithms, develop new products, and create benchmarking datasets that inform precision agriculture recommendations across their client base. Farmers who share their data receive better-performing AI models in return, but they also expose their operational details to companies that may sell insights to commodity traders, input suppliers, or competitors.

The European Union’s Robs4Crops research project identified data control as one of three primary ethical concerns raised by stakeholders during interviews with farmers, regulators, and manufacturers. Farm data privacy regulations vary dramatically across jurisdictions, with some countries offering strong protections and others providing little legal framework for agricultural data governance. The absence of clear industry standards for data ownership, consent, and portability creates a situation where farmers may unknowingly trade their most valuable asset for access to technology, a dynamic that recalls earlier debates about data exploitation in the social media and consumer technology industries. Organizations like the American Farm Bureau Federation have advocated for farm data principles that give farmers transparency and control over how their information is collected, stored, and shared.

Blockchain and distributed ledger technologies offer potential solutions for creating transparent, auditable records of data transactions between farmers and technology providers. The development of open-source robotic platforms and data standards could also reduce farmers’ dependence on proprietary ecosystems that lock them into specific vendors. Addressing data ownership proactively is essential for building the trust that widespread robotic adoption requires, particularly among independent farmers who view their operational knowledge as a core competitive advantage.

Ethical Questions Around Labor Displacement and Rural Communities

The introduction of agricultural robots raises profound ethical questions about the future of farm labor and the communities that depend on it. While proponents argue that robots fill positions that farms cannot otherwise staff, critics point out that automation displaces vulnerable workers, including seasonal laborers and migrant workers, who have few alternative employment options. Research published in AI and Ethics has highlighted concerns that powerful technology companies and agribusinesses might purposely make it more difficult to obtain agricultural visas and encourage stricter immigration policies once robotic alternatives are available. The ethical case for automation is not one-sided; there is a legitimate argument for eliminating jobs that are physically dangerous, repetitive, and poorly compensated, as much agricultural labor falls into the category of work that is “dull, dirty, and dangerous.”

The concentration of robotic technology in the hands of large corporations raises concerns about widening inequality between industrial farming operations and smallholder producers who cannot afford automation. Rural communities that depend on seasonal agricultural employment could face economic decline as robots replace the workers who patronize local businesses, rent housing, and contribute to the social fabric of farming regions. A just transition to robotic agriculture requires deliberate investment in retraining programs, new job creation in areas like robot maintenance and data analysis, and policies that ensure the economic benefits of automation are shared broadly rather than captured exclusively by equipment manufacturers and large landowners. The largely male-dominated profession of computer science and AI development could also exacerbate existing gender disparities in the agricultural sector if women are excluded from the new technical roles that robotic farming creates.

Public attitudes toward agricultural robots are more positive than attitudes toward other controversial agricultural technologies like genetically modified crops, partly because robots do not alter food products directly. A study published in Scientific Reports found that consumers generally view agricultural robots favorably when they understand the environmental and efficiency benefits. This public goodwill provides a window of opportunity for the industry to address labor and equity concerns proactively, before opposition crystallizes into regulatory resistance or consumer backlash.

Safety Standards and Regulatory Gaps

The deployment of autonomous machines in open agricultural environments presents unique safety challenges that existing regulatory frameworks were not designed to address. Unlike factory robots that operate in controlled environments behind safety barriers, agricultural robots share space with human workers, livestock, wildlife, and public roads. Standards organizations including ISO and the American Society of Agricultural and Biological Engineers are actively working on safety and interoperability frameworks for field robots, but multiple sources identify the absence of comprehensive safety standards as a material barrier to commercial scaling. The risk of an autonomous machine injuring a field worker, damaging crops, or colliding with passing vehicles creates liability questions that insurance companies and regulators are still working to resolve.

Interoperability is another critical gap, as robots from different manufacturers often cannot communicate with each other or share data through common platforms. A farmer who purchases a weeding robot from one company and a scouting drone from another may find that the two systems produce data in incompatible formats, requiring manual integration that undermines the efficiency gains that automation is supposed to deliver. Open data standards and communication protocols would allow multi-vendor robotic fleets to coordinate their activities, share information seamlessly, and reduce the total cost of implementing a comprehensive automation strategy. The Food and Agriculture Organization of the United Nations has highlighted agricultural automation as a key lever for food security, adding institutional pressure for governments to develop clear regulatory pathways that enable safe deployment without stifling innovation.

Cybersecurity is an emerging concern as connected agricultural robots become potential targets for hacking, data theft, or ransomware attacks that could disrupt planting and harvesting operations at critical times. The agricultural sector has historically invested less in cybersecurity than other industries, making it potentially vulnerable as its reliance on connected digital systems increases.

From Pilot Projects to Full-Scale Deployment

The agricultural robotics industry is undergoing a crucial transition from early-stage pilot projects to commercial deployment at meaningful scale. Early adopters have proven the return on investment for specific applications like robotic milking, drone scouting, and targeted spraying, and the focus is now shifting toward broad implementation across diverse crops, climates, and farm sizes. The GOFAR Tour 2026, organized by the FIRA agricultural robotics community, is traveling to key agricultural regions worldwide to host events adapted to local crops and challenges, reflecting the industry’s pivot from demonstration to deployment. Solinftec delivered more than twenty Solix Sprayer platforms to major production groups in the grain belt beginning in early 2025, marking the first truly commercial season for large-scale robotic weed management.

Scaling from pilot to production introduces new challenges around supply chain reliability, field service networks, and operator training that are fundamentally different from the engineering challenges of making a robot work in a controlled research setting. The failure of Monarch Tractor illustrates what happens when a company optimizes for technological ambition without building the operational infrastructure needed to support commercial customers. Successful scaling requires partnerships between robotics companies, equipment dealers, agricultural cooperatives, and extension services that can provide the local knowledge and support relationships that farmers depend on. Fully automated operations have already been achieved in warehouse and logistics settings, and the agricultural sector is now applying those lessons to the more variable and unpredictable environment of outdoor farming.

The next phase of commercialization will likely see consolidation in the robotics industry, as well-funded companies with proven products acquire smaller startups or license their technology. The entrance of established agricultural equipment manufacturers like John Deere and CNH Industrial into the autonomous space will accelerate adoption by offering robotic capabilities through existing dealer networks that farmers already know and trust.

Robotics in Controlled Environments and Vertical Farms

While open-field agriculture captures most of the attention in agricultural robotics discussions, controlled-environment agriculture represents a parallel domain where robots are achieving even higher levels of automation and precision. Vertical farms, greenhouses, and indoor growing facilities offer standardized conditions that eliminate many of the variables that make outdoor robotics so challenging, including unpredictable weather, uneven terrain, variable lighting, and diverse weed species. Robots in these settings automate seeding, transplanting, monitoring, climate control, nutrient delivery, and harvesting within tightly controlled parameters that maximize consistency and yield. The modular autonomous robot Thorvald, developed by Saga Robotics, exemplifies the versatility possible in controlled environments, performing tasks ranging from UV-C light treatment for disease control to precision spraying and fruit picking.

These controlled settings serve as testbeds for developing precision robotics technologies that can later be scaled and adapted for open-field applications. The algorithms trained on standardized greenhouse data can be fine-tuned for outdoor conditions, accelerating the development cycle for field-ready robotic systems. The convergence of vertical farming and robotics creates an opportunity for urban and peri-urban food production that reduces transportation distances, minimizes land use, and provides fresh produce year-round regardless of seasonal limitations. The impact of robotics on the workplace is particularly visible in these facilities, where a small team of technicians can manage production volumes that would traditionally require dozens of manual laborers.

Lettuce, herbs, and microgreens are among the crops most commonly grown in fully robotic vertical farms, but ongoing research is expanding the range to include strawberries, tomatoes, and specialty crops that command premium prices. Energy costs remain a significant challenge for controlled-environment agriculture, though the integration of solar panels and energy storage systems is gradually improving the sustainability profile of these operations.

Multi-Robot Fleet Coordination and Swarm Intelligence

The future of agricultural robotics lies not in individual machines working alone, but in coordinated fleets of robots that operate as intelligent swarms across large farming operations. Multi-robot systems divide tasks among specialized platforms, with scouting drones identifying problem areas and directing ground-based robots to intervene with targeted treatments. Fleet coordination algorithms optimize routing, task allocation, and energy management to ensure that every robot is working productively and that no area of the field is overlooked. Research into agricultural swarm intelligence draws on decades of work in multi-agent systems and distributed computing, adapting principles developed for warehouse automation and logistics to the unstructured outdoor environment of a working farm.

Digital farm management platforms serve as the central nervous system for these robotic fleets, aggregating data from all machines, generating actionable recommendations, and allowing farmers to monitor operations from a single interface. The greedy allocation algorithms used in recent multi-robot studies have demonstrated 33% to 37% lower batch completion times compared to traditional assignment methods, suggesting that well-coordinated robotic teams can be dramatically more efficient than individual machines operating independently. The transition from single-robot operations to multi-robot fleets represents the next major capability jump for agricultural automation, enabling farms to achieve continuous, round-the-clock coverage of their fields with minimal human oversight. Communication protocols between robots, including acoustic and radio-based systems, are being developed to maintain coordination even in remote areas where cellular connectivity is unreliable.

The concept of heterogeneous robotic fleets, where different types of robots with different capabilities work together toward common goals, opens the possibility of fully automated farming systems that handle everything from soil preparation to harvest without human intervention at any stage. Realizing this vision requires advances in inter-robot communication, shared spatial awareness, and distributed decision-making that remain active areas of research.

The Investment Landscape and Venture Capital Trends

Venture capital investment in agricultural robotics has surged over the past five years, reflecting growing confidence that the sector is approaching commercial maturity. Startups developing autonomous tractors, weeding robots, drone platforms, and AI-driven crop management systems have collectively raised billions of dollars from investors who see agriculture as one of the largest untapped markets for automation technology. The agricultural robotics market’s projected growth from approximately $18 billion in 2026 to over $40 billion by 2031 creates a compelling investment thesis for venture firms seeking exposure to the intersection of artificial intelligence, sustainability, and food production. Major agricultural equipment manufacturers are also investing heavily, both through internal research and development and through acquisitions of promising startups.

John Deere’s acquisition of Sentera, a drone-based crop analytics company, exemplifies the strategy of established players acquiring specialized technology to integrate into their existing product lines. The competitive landscape is highly fragmented, with global original equipment manufacturers, agtech firms, and innovative startups all vying for market share across different segments and geographies. The cautionary example of Monarch Tractor, which burned through $240 million in funding before collapsing, has introduced greater investor scrutiny around unit economics, path to profitability, and the realism of commercialization timelines in agricultural robotics pitches. Investors are increasingly distinguishing between companies that have demonstrated repeatable, commercially viable deployments and those that remain in the proof-of-concept stage despite years of development.

Robotics-as-a-service models are attracting particular interest from investors because they generate recurring revenue, maintain ongoing customer relationships, and create data assets that appreciate in value as the customer base grows. Government grants and public-private partnerships, such as the U.S. National Science Foundation and USDA partnership on agricultural robotics research, provide additional funding streams that reduce the risk for private investors.

What Farmers Should Know Before Adopting Robotic Systems

Farmers considering the adoption of agricultural robots should approach the decision with a clear understanding of both the potential benefits and the practical challenges involved. The first step is identifying the specific pain points in their operation that robots can address, whether that is labor availability for weeding, the cost of herbicide inputs, the need for more detailed crop monitoring, or the physical demands of repetitive field tasks. Not every robot is suitable for every farm, and matching the right technology to the right application requires careful assessment of crop types, field sizes, terrain characteristics, and existing equipment compatibility. Connecting with other farmers who have already deployed robotic systems provides invaluable practical insight that marketing materials and sales presentations cannot replicate.

The total cost of ownership extends beyond the purchase price of the robot itself to include maintenance, software subscriptions, operator training, field modifications, and the inevitable downtime that occurs when any complex machine encounters problems in a demanding outdoor environment. Farmers should investigate whether robotics-as-a-service options are available in their region before committing to a large capital purchase, particularly if they are uncertain about the long-term fit of a specific technology for their operation. Starting with a lower-cost entry point like a scouting drone or a simple autonomous platform allows farmers to build familiarity with robotic systems before scaling up to more expensive and complex deployments. Connectivity infrastructure, including reliable cellular or satellite internet service, is often a prerequisite for cloud-connected robotic platforms and should be verified before purchase.

Industry events like the GOFAR Tour 2026, university extension programs, and equipment dealer demonstrations offer hands-on opportunities to evaluate different robotic platforms in conditions similar to those on a farmer’s own land. The decision to adopt agricultural robots is not just a technology decision; it is a business decision that requires careful financial analysis, risk assessment, and a realistic timeline for achieving the expected return on investment.

The Road Ahead for Agricultural Robotics

The agricultural robotics sector is poised for a decade of rapid growth and transformation that will fundamentally reshape how food is produced around the world. Cross-platform adoption of robots, satellites, and AI is increasing globally, with the greatest payoff coming when systems are designed from the ground up to be data-driven and scalable. The democratization of robotics through platform integration, user-friendly AI interfaces, and subscription-based access models is making advanced agricultural technology accessible to farms that were previously excluded from the precision agriculture revolution. Regulatory harmonization across countries will be essential for enabling cross-border deployment of robotic systems and creating the large, unified markets that manufacturers need to achieve economies of scale.

The convergence of agricultural robotics with other emerging technologies, including gene editing for crop improvement, satellite-based environmental monitoring, and blockchain for supply chain traceability, will create integrated food production systems that are more resilient, transparent, and sustainable than anything currently in operation. Research initiatives from universities, government agencies, and international organizations continue to push the boundaries of what agricultural robots can perceive, decide, and act upon in the complex and unpredictable environment of a working farm. The agricultural robotics revolution is not a distant future scenario; it is happening now, on farms across six continents, transforming the ancient practice of growing food into a high-technology enterprise that will define the 21st century food system. The farms already running on robotic systems offer a glimpse of what will become standard practice within the next decade.

The challenges that remain are real and significant, from cost barriers and safety standards to ethical questions about labor and data ownership. Solving them will require collaboration among farmers, technology companies, regulators, researchers, and communities that goes beyond simply building better machines to building better systems for deploying them equitably and responsibly.

Key Insights

- A European research project named Robs4Crops identified job loss, moral responsibility, and data control as the three primary ethical concerns raised by farmers, regulators, and manufacturers, highlighting that technical progress must be accompanied by responsible governance.

- According to MarketsandMarkets, the agricultural robots market was valued at USD 16.6 billion in 2024 and is projected to reach USD 51 billion by 2029, reflecting a CAGR of 25.2% that signals a permanent structural shift in farming technology investment.

- Mordor Intelligence reports that the market reached USD 18 billion in 2026, with harvesting and picking robots growing at the fastest rate of 18.9% CAGR as soft-grip technology and machine vision overcome the dexterity challenges of fresh produce handling.

- Solinftec’s first commercial season of its Solix Sprayer robot demonstrated up to 97% herbicide reduction on some properties, conserved 72,000 gallons of water, and delivered up to 10% more biomass and potential yield improvement across corn, popcorn, and soybean operations.

- North America holds 36% to 38% of the global market share, but Research Nester projects Asia Pacific as the fastest-growing region through 2035, driven by Japanese government subsidies, Chinese rural modernization, and rising automation demand across diverse Asian farming systems.

- Carbon Robotics’ LaserWeeder system, now powered by a Large Plant Model containing 150 million labeled plant images, can eliminate approximately 5,000 weeds per minute using thermal energy, enabling growers to start operating in any field or crop within minutes.

- The U.K. government invested £12.5 million in robotics and automation projects in September 2023, and the U.S. NSF partnered with USDA NIFA in April 2024 to advance agricultural robotics research, signaling that public investment is aligning with private sector momentum.

- Dairy robots dominated the market with a 38.1% revenue share in 2024 according to Grand View Research, while UAVs and drones led with 36% of revenue in 2025, illustrating that adoption patterns vary significantly by agricultural sector and farm type.

The agricultural robotics market has crossed the threshold from experimental technology to commercial necessity, driven by forces that are unlikely to reverse. Labor shortages, environmental regulations, and consumer demand for sustainably produced food are creating conditions where automation is not optional but essential for competitive farming operations. The range of available robotic systems now spans every major farming task, from soil preparation and planting through monitoring, weeding, and harvest, with each category maturing at its own pace. Geographic adoption patterns reflect local economic conditions and policy environments, with North America leading in total market share while Asia Pacific accelerates fastest. The industry’s growing pains, including high-profile failures and unresolved ethical concerns, are typical of a transformative technology sector approaching mainstream adoption. The next five years will determine whether agricultural robotics delivers on its promise of making food production more efficient, sustainable, and equitable at a global scale.

| Dimension | Traditional Farming | Robotic Farming |

|---|---|---|

| Transparency | Limited visibility into field conditions; relies on periodic manual scouting and farmer intuition | Continuous, sensor-driven monitoring generates millions of data points per month for real-time visibility into crop and soil conditions |

| Participation | Dependent on available seasonal labor; limited by workforce demographics and migration patterns | Accessible through robotics-as-a-service models; democratized via subscription, reducing capital barriers for small farms |

| Trust | Built on generational farming knowledge and personal relationships with input suppliers and advisors | Requires trust in AI algorithms, data privacy policies, and technology companies with limited agricultural track record |

| Decision Making | Human-driven, experiential; slower response to emerging problems but informed by deep local context | AI-augmented, data-driven; faster response with plant-level precision but dependent on algorithm accuracy and sensor reliability |

| Misinformation | Vulnerable to unreliable marketing claims about crop inputs and outdated agronomic advice from non-expert sources | Generates verified, field-specific data but creates risk of algorithmic bias, opaque model decisions, and vendor lock-in |

| Service Delivery | Constrained by labor availability, weather windows, and human fatigue; inconsistent quality across large acreages | 24/7 operation capability with consistent precision; limited by battery life, mechanical reliability, and field connectivity |

| Accountability | Clear human accountability for farming decisions; familiar legal and insurance frameworks for liability | Distributed accountability across farmers, manufacturers, software developers, and service providers; regulatory frameworks still developing |

Real-World Examples

Solinftec’s Solix Deployment Across Brazilian Sugarcane Operations

The sugar-energy plant Cruz Alta in Olímpia, São Paulo, owned by French group Tereos, began deploying two Solix AG Robotics platforms in April 2024 to spray herbicide on sugarcane crops. According to Revista Pesquisa FAPESP’s coverage, the initial trials produced a 50% reduction in pesticide use, with the AI-powered computer vision system differentiating actual crops from weed species and applying herbicide selectively rather than broadcasting across the entire field. The Solix platform operates on solar-charged batteries and runs 24 hours per day, covering large acreages that would require multiple tractor-sprayer combinations under conventional approaches. Critics note that the technology was initially optimized for grain crops and required adaptation for sugarcane’s height and row spacing, demonstrating that transferring robotic solutions between crop types is not always straightforward.

Naïo Technologies’ Ted Robot in French Vineyards

Naïo Technologies partnered with the prestigious Château Mouton-Rothschild to deploy its Ted vine-tailored robotic weed killer across their vineyard operations, as documented by Built In. The electric robot is shaped like an inverted U, rolling over and around vine rows while using RTK satellite navigation and drone-generated field maps to maintain course accuracy. Industry-standard blades and finger weeders along its base remove weeds mechanically, decreasing the need for herbicides in vineyards where chemical residues can affect wine quality and terroir. The system reduces labor costs for one of the most labor-intensive vineyard tasks, though its effectiveness is limited to relatively flat terrain, and its $35,000 price point remains a significant investment for small vineyard operators who grow high-value but low-volume crops.

Carbon Robotics’ LaserWeeder in U.S. Specialty Crops

Carbon Robotics deployed its LaserWeeder across high-value specialty crop operations in the western United States, using thermal energy to destroy approximately 5,000 weeds per minute without soil disturbance or chemical application, as reported by Farm Equipment Magazine. The company’s Large Plant Model, trained on 150 million labeled plant images, enables rapid deployment in new crops and fields by allowing operators to update target classifications with a single tap. The LaserWeeder has proven particularly popular for high-value crops like lettuce and onions where organic premiums justify the investment and where weed pressure is highest. The economics have been slower to justify adoption for lower-value row crops like corn and soybeans, where herbicide costs are relatively modest and the financial return on a capital-intensive robotic system takes longer to materialize.

Case Studies

John Deere’s Autonomous 8R Tractor Program and Sentera Acquisition

John Deere has pursued agricultural autonomy through a multi-decade strategy that began with its AutoTrac GPS steering system in 2003 and has progressed to its autonomous 8R tractor kit, which retrofits existing tractors with cameras, sensors, and AI navigation. The company acquired Sentera, a drone-based crop analytics firm, to integrate aerial intelligence with its ground-based autonomous platforms and create a comprehensive precision agriculture ecosystem. The 8R autonomous system allows farmers to start tractor operations remotely and monitor progress through a mobile application, reducing the time farmers spend on repetitive driving tasks and enabling them to manage multiple field operations simultaneously. Despite these advances, the premium pricing of $500,000 or more for the tractor and autonomy kit combination limits adoption to large-scale operations with sufficient acreage to justify the investment, and the system still requires a human supervisor available to intervene remotely, falling short of the fully unsupervised autonomy that the industry envisions.

Solinftec’s First Commercial Solix Season in the U.S. Grain Belt

Solinftec completed its first commercial season of Solix Sprayer robot deployment in the U.S. grain belt during 2024, delivering more than twenty platforms to major production groups growing corn, popcorn, and soybeans, as documented in the company’s official announcement. The robots applied 15,089 gallons of product during the season while conserving 72,000 gallons of water, achieving herbicide reductions of up to 97% on heavily infested properties and generating up to 10% more biomass and potential yield. The launch of the Solix docking station at the Farm Progress Show in August 2024 promised to enable 100% autonomous operation throughout the growing season by eliminating the need for manual refills. The scale of deployment, while impressive for a first commercial season, remains modest relative to the millions of acres of grain production in the Midwest, and questions about long-term reliability, repair turnaround times, and performance consistency across different soil types and growing conditions require multiple seasons of data to resolve fully.

The Collapse of Monarch Tractor: A Cautionary Industry Case Study

Monarch Tractor launched its electric, driver-optional smart tractor in 2023 with over $240 million in funding and a valuation exceeding half a billion dollars, positioning itself as a disruptor in the autonomous agricultural equipment market. As reported by Futurism, the company burned through its entire capital reserve, laid off its whole workforce in late 2025, and vacated its Livermore, California headquarters by early 2026. The gap between the technology’s theoretical promise and the practical realities of manufacturing, distributing, and supporting complex agricultural equipment at scale proved insurmountable within the company’s financial runway. The Monarch case has become a reference point for the agricultural robotics industry, illustrating that hardware startups face fundamentally different challenges than software companies, including high manufacturing costs, lengthy certification processes, seasonal demand patterns, and the need for nationwide service infrastructure that takes years and significant capital to build.

Frequently Asked Questions on Agricultural Robots

Agricultural robots can handle a wide range of farming operations including planting, seeding, weeding, spraying, harvesting, soil monitoring, crop scouting, milking, feeding livestock, and environmental sensing. The specific capabilities depend on the robot’s design, with specialized platforms targeting individual tasks and multi-purpose modular systems offering interchangeable attachments for different seasonal needs. Autonomous tractors handle field preparation and transport, while drones provide aerial surveillance and targeted application from above.

Costs vary dramatically depending on the type and scale of robotic system, ranging from approximately $18,000 for a spray drone to over $350,000 for a large-scale autonomous weeding platform. Autonomous tractor systems can exceed $500,000 when the base tractor and autonomy kit are combined. Robotics-as-a-service subscription models offer lower entry points by converting capital expenditure into per-acre or seasonal operating fees, making automation accessible to farms that cannot afford outright purchases.

The payback period depends on farm size, crop type, and the specific application being automated, but typical ranges are 2 to 4 years for commercial deployments. A 500-acre vegetable operation deploying robotic weeding and drone monitoring can save over $150,000 annually, achieving payback in approximately 2.5 years. High-value specialty crops like berries and lettuce offer faster returns due to higher labor costs and organic premiums that reward chemical-free production.

Robotic systems use computer vision and AI to identify individual weeds and apply treatments only where they are needed, eliminating the waste inherent in broadcast spraying across entire fields. Some systems use mechanical removal or laser-based thermal energy instead of chemicals entirely. Field trials have demonstrated herbicide reductions ranging from 50% to 97% depending on the crop, weed pressure, and specific robotic platform used.

Yes, several robotic platforms are specifically designed for small and mid-sized farming operations, with compact form factors and lower price points. The Naïo Oz weeding robot costs approximately $35,000 and is designed for market gardens and small organic farms. Robotics-as-a-service models further improve accessibility by eliminating the need for large capital investments and providing technical support that small operations may lack internally.

The impact on farm labor depends on how robotic systems are implemented and what support structures are in place. Robots primarily fill positions that farms struggle to staff due to labor shortages, physically demanding conditions, and low wages, rather than directly displacing workers from jobs they want to keep. New roles in robot operation, maintenance, data analysis, and fleet management are emerging, though they require different skills than traditional farm labor and may not be accessible to all displaced workers without retraining.

Outdoor agricultural environments present significant challenges for robotic systems, including dust, moisture, extreme temperatures, variable lighting, uneven terrain, and crop canopy obstruction of sensors. Modern agricultural robots are engineered for these conditions with ruggedized components, weather-resistant enclosures, and redundant sensor systems. Reliability continues to improve with each generation, though downtime for maintenance and repairs remains a practical consideration that farmers should plan for.

Yes, many agricultural robots are designed to operate continuously around the clock, including during nighttime hours when certain tasks may actually be more effective. Solinftec’s Solix Hunter module is specifically designed for nocturnal pest control operations. Camera-based weeding systems using controlled illumination can be more accurate at night because they eliminate the variability of natural sunlight that affects daytime image processing.

Drones serve as the aerial intelligence layer of a robotic farming system, providing rapid, wide-area surveillance of crop health, pest infestations, irrigation status, and plant growth patterns. They use multispectral and thermal sensors to detect problems invisible to the human eye. Drones also perform precision spraying, seeding, and mapping operations that guide the deployment of ground-based robots to specific areas requiring intervention.

Robot-generated data feeds into farm management platforms that provide real-time dashboards, historical trend analysis, and AI-driven recommendations for input optimization. This data includes soil health metrics, plant population counts, weed density maps, pest identification records, and yield predictions. Farmers use these insights to make informed decisions about irrigation, fertilization, pest management, and harvest timing, while robot manufacturers use aggregated data to train and improve their AI models.

Safety standards for agricultural robots are still being developed by organizations like ISO and the American Society of Agricultural and Biological Engineers. Current regulations vary by country and often borrow from existing machinery safety frameworks that were not specifically designed for autonomous outdoor platforms. The absence of comprehensive, internationally harmonized safety standards is identified as a material barrier to commercialization by multiple industry analysts.

The market is projected to grow from approximately $18 billion in 2026 to over $40 billion by 2031, with some estimates projecting over $120 billion by 2035. Trends driving this growth include multi-robot fleet coordination, improved AI perception systems, declining sensor costs, and the expansion of robotics-as-a-service models that make automation financially accessible to more farmers. The integration of robotics with satellite imagery, gene editing, and blockchain traceability will create increasingly sophisticated food production systems within the next decade.

Farmers should begin by identifying their most pressing operational challenges and evaluating which robotic solutions address those specific needs. Attending industry demonstrations like the GOFAR Tour 2026, consulting university extension services, and connecting with farmers who have already deployed robots provides practical insight. Starting with a lower-cost entry point like a scouting drone before scaling to more expensive ground-based platforms reduces financial risk and builds operational familiarity.